“Few commodities cycle like lithium does.”

From staggering highs to abrupt plunges, and now renewed upward pressure, the market for lithium carbonate – the lithium chemical used in lithium iron phosphate (LFP) batteries – has been anything but predictable. These swings have left investors, manufacturers, developers, and policymakers trying to understand whether the market is simply maturing—or whether volatility is becoming a permanent feature of the battery economy.

The answer is likely both.

It is fair to argue that the lithium market today is more mature than it was during the 2021–2022 price shock following the invasion of Ukraine which sent fuel prices soaring. Supply has expanded, buyers are more sophisticated, and the industry has learned hard lessons about overreliance on short-term market signals. But market maturity does not automatically mean price stability. As batteries become central to electric vehicles, grid storage, data centers, and industrial electrification, lithium-ion supply chains are becoming more strategically important—and therefore more exposed to geopolitical, policy, and trade-driven disruption.

The Anatomy of Lithium-ion Volatility

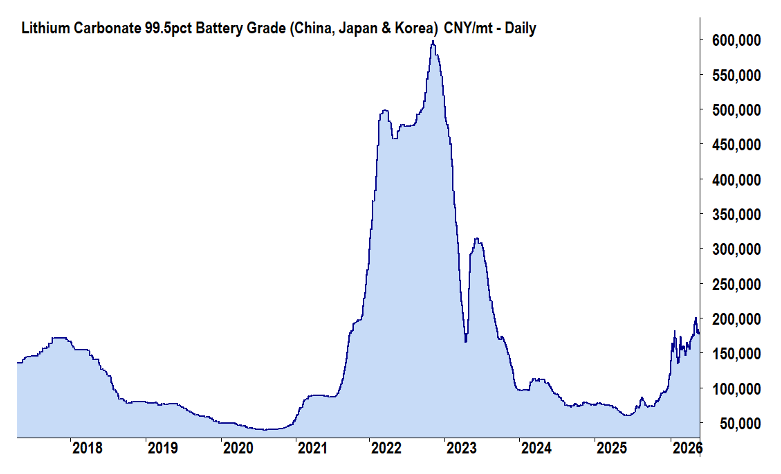

The 2022 lithium price shock was extraordinary, but it was not random. Battery demand surged as elevated gas prices caused consumers to turn to EVs, automakers rushed to secure materials, and market participants became increasingly concerned about access to lithium, nickel, graphite, and cobalt. Prices rose quickly as buyers competed for limited near-term supply.

The market then responded the way commodity markets often do: capital rushed in, supply expanded, inventories built, and prices collapsed. By late 2024 and 2025, the industry was dealing with the opposite problem—oversupply, project delays, weak margins, and uncertainty about which producers could survive a lower-price environment.

This is where some observers argue that the market has learned its lesson. They suggest the 2022 shock is unlikely to repeat, and that recent price increases are signs of a more balanced, more mature lithium market.

That view may be partially right—but it is incomplete.

Lithium-ion batteries are not just another commodity market. They sit at the intersection of industrial policy, global trade, national security, energy security, and climate strategy. That means prices are not shaped by supply and demand alone. They are shaped by speculation, tariffs, export controls, permitting delays, domestic-content rules, geopolitical conflict, and the ability of dominant market players to expand or restrict supply at strategic moments.

A more mature lithium market may reduce some forms of volatility, but it does not eliminate the deeper structural risks. If anything, the strategic importance of batteries increases the likelihood that governments and large market actors will continue to intervene in ways that make long-term cost planning difficult.

Why the “This Won’t Happen Again” Argument Misses the Point

The question is not whether lithium carbonate will repeat the exact 2022 price spike. It may not.

The better question is whether lithium-ion batteries will remain exposed to unpredictable cost shocks. On that point, the answer is almost certainly yes.

There are several reasons.

First, lithium supply remains cyclical. When prices fall too far, projects are delayed, mines are idled, and investment slows. When prices rise again, buyers rush back in, financing reopens, and speculation returns. This boom-bust dynamic is not a sign of a broken market; it is how many commodity markets behave.

Second, the supply chain remains geographically concentrated. Even when raw lithium production diversifies, processing, refining, graphite supply, cell manufacturing, and component manufacturing remain heavily dependent on China. That concentration creates exposure to policy shifts, export controls, sanctions, tariffs, and trade disputes.

Third, battery demand is no longer driven by one end market. EVs, stationary storage, grid infrastructure, consumer electronics, industrial electrification, and AI-driven data center growth are all competing for battery supply. When multiple sectors depend on the same chemistry family, shocks in one market can ripple across the entire supply chain.

Fourth, policy risk is increasing. Tariffs on lithium-ion batteries and graphite, Foreign Entity of Concern (FEOC) rules, domestic-content requirements, and critical-mineral security policies all affect the true landed cost of batteries. These measures may support domestic manufacturing over time, but in the near term they can add cost, complexity, and uncertainty.

This is why the lithium-ion market can become more mature and still remain volatile. Maturity does not remove geopolitical risk. It does not remove trade risk. It does not remove speculation. And it does not remove the challenge of building a battery supply chain around materials that remain strategically contested.

The $40/kg Tipping Point

Global battery research firms point to $40/kg for when lithium carbonate reaches an important economic threshold. When lithium carbonate moves toward or beyond that level, lithium-ion batteries achieve near-cost parity with sodium-ion batteries.

At $40/kg, LFP’s lowest-cost argument starts to evaporate and it can be more evenly evaluated across performance and economic attributes to sodium. Beyond Wh/L and $/kWh, those attributes at least for grid-scale storage include system-level round-trip efficiency, operating temperature range, cycle life, lifetime energy throughput, and more.

With grid storage, compared to other segments, the winning technology is the one that delivers the best lifetime economics across safety, thermal management, augmentation, degradation, usable capacity, maintenance, supply security, and installation constraints.

There are also many hidden costs of LFP that would get more scrutiny with cost parity. For example, a project may secure an LFP system at an attractive price today, but stationary storage assets are not always one-time purchases in practice. Over the life of a project, systems may require augmentation, replacement modules, or other capacity-maintenance measures to preserve contracted performance as batteries degrade.

That matters because future augmentation does not necessarily happen under today’s pricing conditions. A developer may benefit from a low-cost LFP procurement cycle at the beginning of a project, only to face a very different cost environment several years later when augmentation is required. If lithium carbonate, graphite, cell, tariff, or logistics costs have moved materially by then, the lifetime economics of the system can look very different from the initial quote.

This is another reason sodium-ion should not be evaluated only on upfront cell cost. For stationary storage, the more relevant question is whether the chemistry can deliver predictable cost, safety, and performance over the full life of the asset.

That means $40/kg should be viewed less as the point where sodium-ion first becomes competitive, and more as the point where the industry is forced to evaluate lithium-ion and sodium-ion on a more even playing field.

Below that threshold, lithium-ion’s scale advantage can obscure system-level tradeoffs. Above it, the cost volatility of lithium becomes harder to ignore. At that point, buyers begin asking a different question: not “What is the cheapest cell today?” but “What chemistry gives us the most predictable, bankable, and secure cost structure over the life of the asset?”

The Strategic Shift: Alsym’s Na-Series

Since its founding Alsym saw problems with the way lithium-ion battery materials are sourced, refined, manufactured, traded, and used. The answer was sodium iron pyrophosphate (NFPP) because we saw it as a viable technology based upon globally abundant sodium that could also drop-in to existing lithium-ion manufacturing and integration infrastructure.

Sodium is widely available, geographically distributed, and not exposed to the same strategic bottlenecks as lithium. Iron and phosphorus are also far more abundant and globally accessible than many incumbent battery materials. Together, they create a chemistry platform that is inherently better insulated from the tariff, export-control, and mineral-security risks that continue to affect lithium-ion batteries.

Beyond the supply chain, the Na-Series presents a very compelling package for benefits for grid-scale battery system operators that culminate into a chemistry providing the safest, most stable, and most bankable cost structure over time.

A more resilient energy storage future will depend on chemistry diversification, localized supply chains, and technologies designed around the real requirements of stationary storage—not the assumptions of the EV market.

The Alsym Na-Series is built for that future.

(Image sourced from livewire markets/originally Shangai Metals Market)